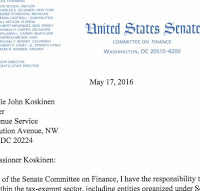

Last November I drew attention to a letter that Senator Orrin Hatch (R Utah and Chair of the Senate Finance Committee) sent to a handful of private nonprofit museums founded by individual living collectors. His goal was to assess whether these institutions were providing enough of a public benefit to justify their nonprofit status.

Yesterday, Independent Sector’s Daily Digest linked to the letter Senator Hatch submitted to the IRS summarizing his conclusions from these inquiries, including a list of his questions and the museums’ responses. No one working in museums will be surprised to hear that the Senator received a wide variety of responses to his inquiries about open hours, number of visitors, admission fees, partnerships with/loans to other museums, donor relations, policies on restricted gifts, ownership of the museum’s land and buildings, and grants bestowed by the museum.

Yesterday, Independent Sector’s Daily Digest linked to the letter Senator Hatch submitted to the IRS summarizing his conclusions from these inquiries, including a list of his questions and the museums’ responses. No one working in museums will be surprised to hear that the Senator received a wide variety of responses to his inquiries about open hours, number of visitors, admission fees, partnerships with/loans to other museums, donor relations, policies on restricted gifts, ownership of the museum’s land and buildings, and grants bestowed by the museum.

The Senator clearly has reservations about some of the answers he received, particularly those that reveal “highly irregular schedules,” restricted hours and reservation systems that require visitors to make arrangements weeks or months in advance. “Some of the museums I surveyed,” he notes, “are not readily accessible by the general public.” While Hatch states that nothing he uncovered is cause for revocation of tax-exempt status, he feels the factors he examined “do raise questions about the nature of the relationship between the donor and museum that perhaps merit further scrutiny. “Despite the good work that is being done by many private museums,” the Senator concludes, “I remain concerned that this area of our tax code is ripe for exploitation.” He closes the letter by asking that the IRS Commissioner respond with details on how the service is providing “sufficient guidance” to private (by which I think he means “founder/donor-driven”) museums.

I bring this letter to your attention because it is one more “signal” (futurist short hand for “piece of news providing supporting evidence of a trend”) of growing threats to museums’ nonprofit status. Related signals I’ve explored on the Blog include:

The many challenges faced by Kansas museums, including multi-year funding cuts, attempts to eliminate sales-tax exemptions, elimination of funding for the state arts commission, and proposals to eliminate tax-exempt status of nonprofits that compete with for-profits. (I wrote that post in 2013. I think we are ready for another summary, this time on the forces buffeting museums in Illinois.)

The growing gap between the way society and donors view nonprofits that provide basic social services, and those that dedicated to culture and science.

The IRS’s revocation, in 2011, of the nonprofit status of about 275,000 organizations that didn’t file appropriate paperwork. Not that thinning the ranks of non-reporters was a bad step in and of itself, but it’s yet another indicator of heightened scrutiny of nonprofits.

The current economic and political climate only makes this issue of nonprofit status more fraught. One person at the annual meeting, throwing out a mini-scenario of a plausible future, remarked “I can totally imagine that if Donald Trump is elected, and is trying to balance the federal budget, he could direct the IRS to say that only accredited museums are eligible for tax exempt status” [in order to put more organizations back on the tax rolls.]

All of which is to say, we can’t take tax exempt status—a bedrock of museum existence in the US—for granted. Others can, and are, questioning what museums do to justify this public subsidy. In yesterday’s post I waxed enthusiastic about the potential museums to convince funders of our ability to make the world a better place. Let’s not forget that we need to make that case to policy makers as well.

All of which is to say, we can’t take tax exempt status—a bedrock of museum existence in the US—for granted. Others can, and are, questioning what museums do to justify this public subsidy. In yesterday’s post I waxed enthusiastic about the potential museums to convince funders of our ability to make the world a better place. Let’s not forget that we need to make that case to policy makers as well.

Upcoming Events

-

Basics of Fundraising Virtual Workshop

Event Date:Presented by: American Association for State and Local History (AASLH) -

-

From Idea to Acceptance: How to Submit a Winning Annual Meeting Session Proposal

Event Date:Presented by: American Alliance of Museums -